Independent Sponsor Series – Capital Provider Spotlight: A Conversation with Paul Moffatt of Encore One (Part One)

To help businesses, investors, and deal professionals better understand the evolving independent sponsor landscape, Robert Connolly – a partner in LP’s Corporate Practice Group and leader of LP’s Independent Sponsor team – shares a series of conversations with independent sponsors, capital providers and other professionals.

Below is his conversation with Paul Moffatt, Vice President of Encore One, a private holding company that historically acquired middle market businesses poised for long-term success and has recently shifted strategies to focus on direct minority equity co-investments alongside leading sponsors. With over 16 years of experience in commercial banking and sponsor finance, Paul sources and evaluates potential investments, structures and negotiates transactions, and works with portfolio companies. In this first of a two-part Q&A, Paul explains Encore One’s investment strategy, relationship with independent sponsors, and approach to deal terms and structure. In part two, he describes the ideal independent sponsor, differentiating factors, and market trends.

The responses below have been edited slightly for brevity and clarity.

Can you provide an overview of Encore One and its investment policy?

Encore One is a Minnesota-based, family-owned investment holding company. We’re a direct investment arm within a more diversified family office. We have affiliates that do fund manager investing, public market investing, and real estate investing. We’re related to the family’s original source of wealth – a national construction and real estate development firm with an 80-year family business history. The patriarch had the idea to keep the construction firm in the family for generations, so it’s owned by two family trusts, then to diversify that family wealth away from construction this diversified family office was set up dating back to the late ‘90s.

Encore One, historically pursued our own majority control buyouts, so we’ve been on the sponsor side of the table as far as the equity is concerned. Over time, we’ve remained a small group, and yet the competition has come down-market from other investors, including family offices, private equity, and a proliferation of independent sponsors.

About a year ago, we made the strategic decision to pursue minority equity co-investments in other sponsor-led deals and buyouts to deploy capital and diversify faster than we can do one majority buyout deal at a time in this competitive environment with our team resources. We maintain a long-term legacy portfolio that’s been held since the early 2000s, which continues to grow and do well, but we’re increasingly concentrated in a few names. A co-investing strategy will allow us to deploy capital and diversify faster while maintaining a professional approach with a small team and has provided us the exposure to the

independent sponsor ecosystem.

Our investment philosophy is to partner with quality sponsors, management, and seek alignment with the investment group, providing minority equity capital for leading middle market companies. We are very relationship-driven, as well as focused on institutional quality underwriting, but we are flexible. We are not part of a committed fund, so we don’t have a predetermined timeline for exits. We generally can move quickly and don’t have to raise capital for individual deals. We have ample resources.

What role do independent sponsor transactions play in your overall investment strategy?

They have a very significant role. That’s about one-third to half of our deal flow and the deals we commit to and close. Previously, we pursued our own majority control buyouts, usually negotiating directly with business owners, which is one audience and philosophy or approach to investing and creating a diversified portfolio. Pursuing relationships with sponsors and independent sponsors is an entirely different audience and sales development channel.

At first, upon this pivot, I wasn’t sure where we would find opportunities, but I’ve been pleasantly surprised at not only the number but also the quality of sponsors and investment opportunities the co-investment strategy presents. So, independent sponsors are a significant part of our investment strategy. I’ve enjoyed getting to know the advisors involved in that ecosystem, in addition to different sponsors’ approaches and backgrounds.

How does your approach differ from other capital providers investing in independent sponsor deals?

Our approach differs from other investors – whether other family offices, high-net-worth individuals, or committed funds – in that our independent sponsor deals are fairly institutional, given our collective experience at Encore One as well as obligation to the trusts that own Encore One. We’re fiduciaries for a pool of family capital allocated to our group, so we need to make well-informed investment decisions that we can defend and stand behind. Our approach is not entirely unique but may differ from some.

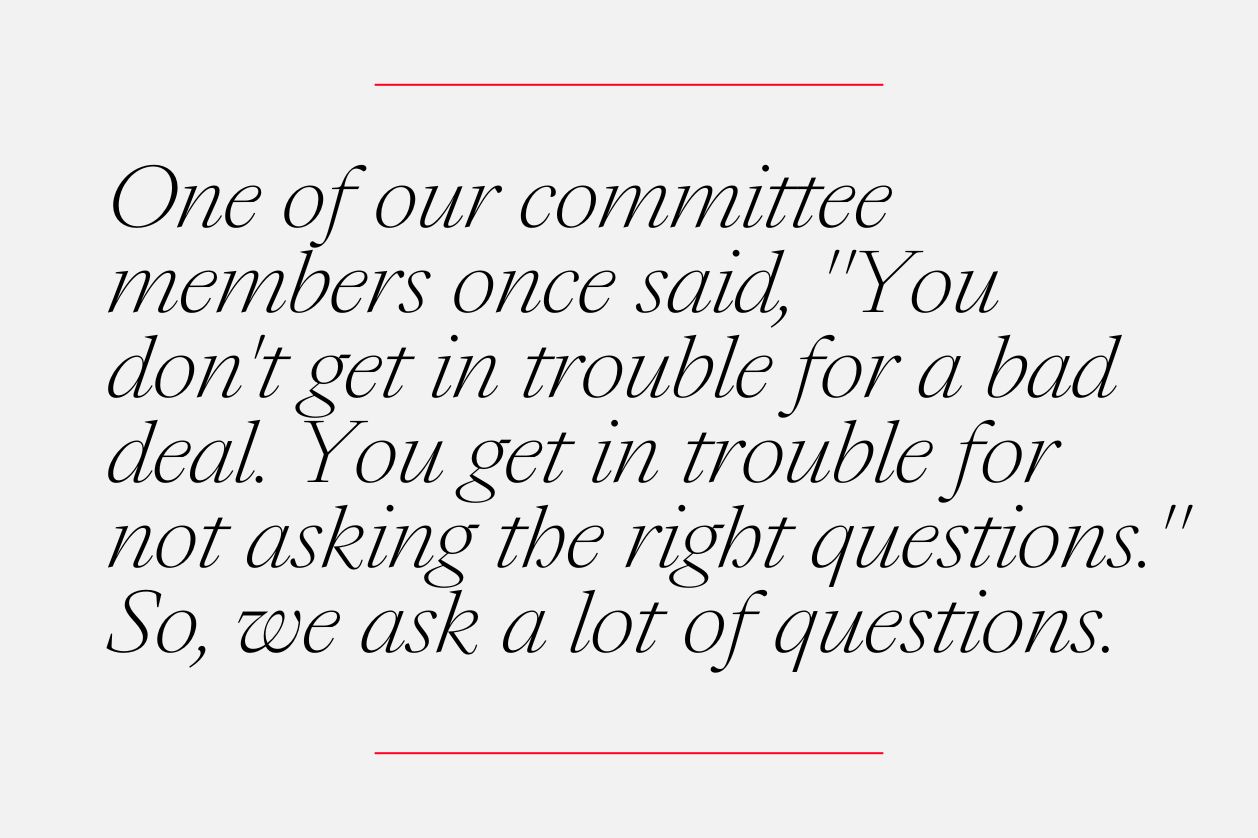

One of our committee members once said, “You don’t get in trouble for a bad deal. You get in trouble for not asking the right questions.” So, we ask a lot of questions. We’re not creating any new diligence streams;

we’re leaning on the sponsor and what they can provide from legal, accounting, and commercial market studies. However, we expect those items and third-party reports to be available for us to review and ask

questions. Our approach is thoughtful. We also value relationships and transparency.

I’ve run into some experienced independent sponsors and investment management companies that historically might have had a stable of reliable high-net-worth families or individuals who have supported their deals over many years. We start a relationship because some of their existing LPs might be aging and don’t have the capacity to monitor and maintain an investment for another 5-10 years with that flexible time horizon. We are introduced as potential new investors to join that stable of long-term or flexible investors.

We ask more questions than the old guard might have previously pursued, but it creates a good opportunity to get to know one another and start a working relationship. It’s not that they don’t have the information available; they just previously may not have had to discuss certain issues that either go without saying or prior LPs and investors may not have picked up on.

We’re a small group. There are three of us and a small board that acts as our de facto investment committee. We’re able to work quickly. So, while the expectations are institutional, there’s a fraternal informality to it as well. We’re relationship-driven.

After we get the sponsors’ base case and their target case, we usually put it into our own model using their financial information and taking a slice for ourselves, which is probably more conservative, but it’s a prudent approach as a minority equity co-investor to be extra comfortable with the opportunity and the growth prospects of that business to drive good returns, hopefully in excess of 20% IRRs.

What are your investment criteria for deal selection?

We’re agnostic with our investment criteria deal selection although stick to businesses we understand. We’re targeting lower middle market companies that can drive adequate returns. They tend to have an EBITDA range of about $5-25 million, and that’s reflective of our pocketbook. So, for any individual investment, our check size would be $2.5-10 million per investment. With several opportunities and our diversification goal, the sweet spot will probably end up at around $3-7.5 million, depending on the current activity level and the opportunities we’re seeing. We aim to make 3-5 minority equity co-investments per year with any type of sponsor, including independent sponsors.

Within our group at Encore One, we’re not often LPs in other private equity funds. Many of our opportunities come from traditional independent sponsors, investment managers, and other family office groups. That said, we see the private equity fund-led buyout deal occasionally, where they might invite new third-party co-investors who aren’t existing LPs in funds. Those deals usually have a way of finding us, and we’re not necessarily marketing or soliciting those opportunities, but they are of high quality which the independent sponsor universe should keep in mind, as they are also hunting the same sources of capital.

Given our target check size, we stick to what we know, which tends to be mature business services, financial services, healthcare services, manufacturing, industrial, logistics, and value-added distribution sectors. We’d like some technology and healthcare in our portfolio, but we haven’t found the right one yet. It may require the right sponsor, which can provide leadership in those industries and segments we have less experience with.

We try to avoid companies that are on the same economic cycle as real estate development and construction, given our relationship with our affiliate sister company. That would be the biggest no-go. Other non-starters are industries where we’re overexposed in the industry or market. Otherwise, we’re looking at the quality of diligence, the sponsor, the commitment from the individual sponsors, and market terms. The biggest concerns – which I think anybody would be concerned with – are customer

concentrations, being captive to a single OEM or vendor, as well as leadership succession.

When it comes to structure, economics, and control of independent sponsor deals, how do you facilitate an alignment of interest between your family office and the independent sponsor?

The most attractive elements we look for when assessing the quality of the business opportunity are whether it’s proprietary or a uniquely attractive entry price; then does it involve a sponsor with significant prior experience from different firms or another industry, operations, deal-making, or a roll-up integration experience. Because of the sheer number and quality of opportunities we see, we have to make decisions – and some of those might be no-go decisions – on the margins of the set-up of an investment opportunity.

We have a finite amount of time and capital to respond to the number of investments we see. A big alignment of interest element that we evaluate is the sponsor’s committed capital, which can be tough for some and not a big deal for others, depending on their life stage and prior experience. Have they previously been a partner in a private equity firm with marketable success and can contribute significant capital? That’s one piece.

Sometimes, we find alignment with other family offices where there might be an investment management team, and that single-family office will commit a significant amount of capital. There are mitigants to lack of available sponsor capital as well, such as whether it’s a highly engaged seller with a substantial rollover position, and the roll of success fees. Beyond that, other mitigants are minority rights, roles, and responsibilities. Those elements of an operating agreement might also provide some additional alignment.

But the big one that answers a lot of questions is the amount of committed capital. So, carry has a benefit of upside alignment and motivation, but as a minority owner, it’s nice to see if there’s some downside alignment if things aren’t going well and that there’s a significant commitment of time dedicated to a particular investment.

How do you typically approach economics with independent sponsors?

Maybe it’s an unfair comparison, but we also see deals where we’re comparing the independent sponsors to another family office-led deal with an experienced investment team. We could be comparing the independent sponsor to a deal where we have a strong pre-existing relationship, or it might be a sophisticated private equity fund that has operating partners and a well-detailed value creation plan for a business, and they’re committing not only GP dollars but also fund dollars as well to that deal. So, that makes it difficult for independent sponsors to compete in that respect.

Whether an independent sponsor opportunity stands out among other opportunities depends on the capital commitment, the amount or roll of success fees so they’re not taking money out to keep the lights on, attractive or reasonable management fees, perhaps with a cap, and a carry structure that’s within market and a reflection of the amount of effort to be put into the successful development of the platform investment. We’ve seen all tiered carry structures, such as over 30% over 3.5 times MOIC on the high end. We’d also like to see a lower number on the downside in those instances. We’ve seen the straight 20% carry, which is easy, but probably lacks alignment on the downside. We’ve seen some attractive structures typically from traditional private equity funds or individuals acting as independent sponsors who aspire to become a fund manager and are looking to get a few deals under their belt for which they can have attribution. Those individuals usually present attractive deals and carry structures that are less than 20% carry. Again, something to keep in mind from the competition of capital raising perspective is that there are others out there that potentially aren’t charging as much. It’s nuanced. Every situation is different and they’re all relative.

Are you firm or flexible on deal terms depending on the sponsor and opportunity?

Yes, we’re absolutely flexible. For instance, if we have 20% of the equity investment and we’re the largest individual check, we might expect board observation rights in that situation. However, in a different situation where we’re only 5% of the equity, there are other high-quality investors we’re aligned with, and it’s a larger deal for a sophisticated company with a strong management team, we would expect to be covered by the rights that other minority investors have who would be good stewards of our capital protecting our investment. We’re flexible on specific deal terms.

Overall, though, we are looking for a relationship that includes transparency. Different sponsors, depending on their experience, might come at this differently. Sometimes, the sponsor does not want us to know who the other investors are. In other cases, they’re very forthright. They hold investor meetings, and during due diligence, there’s a lot of visibility between management and the seller (or whoever the operating partner will be) as well as capital providers and the seller. To the extent that a sponsor can, with the proper NDAs and non-circumvention agreements in place, provide that level of transparency, it helps to grease the skids and

ease any tension.

If any investor (minority or otherwise) feels like they have access and an open dialogue with transparency, that a sponsor is not obfuscating or hiding the equity source from their seller or their management team, and they’re explaining that they are an integrator and a consolidator who’s sponsoring or championing a deal, that’s great. I wouldn’t think any investor would want to get into a situation where they aren’t aware of any of the other investors and somehow find out after the close that the seller is otherwise unaware that there is a group or syndication of investors that are standing behind this individual sponsor. Open dialogue is good for transparency and success. More eyes and smart people looking at and strategically supporting an investment is a better place to operate from.

Any organic opportunity that makes sense, where the sponsor can facilitate transparency between investors and the seller’s management team, recognizing that it takes time and some finesse to set up and facilitate, presents an ideal situation. Maybe it’s not every investor; maybe lead investors can communicate and share thoughts and feedback with other investors but understanding that it’s all very tenuous and the pressure’s on with the independent sponsor sitting in the middle of all that. If possible, that’s a great position to operate from.

How do you view and negotiate protective covenants and rights with independent sponsors?

We’re always seeking clear knowledge of the tag- and drag-along rights, preemptive rights, exit rights, and transfer rights. I don’t know that every investor gets into the weeds on that, but we would certainly review those to our satisfaction and share with our investment counsel as well, not necessarily looking to make any changes or negotiate something different, but to have our eyes wide open and understand where we are in the capital stack, the opportunity, the sponsor experience, etc.

For more information on Paul Moffatt, visit his bio. For more information on Encore One, visit their website.

To read other articles in this series, please see here: Insights | LP (lplegal.com)Interested in participating in a future interview series? Please contact Robert Connolly.